Deets On Wealth Redistribution Options and Antitrust Breakup Act

Deets On Wealth Redistribution Options and Antitrust Breakup Act

Deets On The Fair Deal

Deets On Wealth Redistribution Options and Antitrust Breakup Act

Deets On Wealth Redistribution Options and Antitrust Breakup Act

Whereas, it is the duty of the United States government to promote the general welfare, ensure economic stability, and address income inequality; and

Whereas, the current tax system fails to adequately achieve these objectives and is in need of comprehensive reform; and

Whereas, the following measures are proposed to address wealth redistribution, national economic surplus, and economic stabilization;

Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled,

Section 1: Wealth Tax Implementation

1.1. A progressive wealth tax shall be levied on individuals with net assets exceeding $50 million, with rates ranging from 1% to 5% based on wealth brackets.

1.2. The proceeds from the wealth tax shall be used to fund social welfare programs, infrastructure projects, and initiatives aimed at reducing income inequality and promoting economic opportunity.

1.3. Exemptions and Deductions:

Establish criteria for exemptions or deductions from the wealth tax for certain assets, such as primary residences, retirement accounts, and small businesses, to prevent undue burden on middle-class families and encourage productive investment.

Consider implementing a threshold below which wealth tax does not apply, ensuring that the tax primarily targets the wealthiest individuals while minimizing administrative complexity and compliance costs.

1.4. Enforcement and Compliance:

Allocate resources for enhanced enforcement measures to ensure compliance with the wealth tax regulations, including audits, asset evaluations, and penalties for evasion or underreporting of assets.

Implement reporting requirements for financial institutions and wealth management firms to facilitate monitoring of high-net-worth individuals' assets and detect potential tax evasion or offshore wealth concealment.

1.5. Interjurisdictional Coordination:

Coordinate with international tax authorities and organizations to address challenges related to cross-border wealth taxation, including coordination of tax treaties, information exchange agreements, and measures to prevent tax base erosion and profit shifting.

Advocate for global standards and best practices in wealth taxation to promote tax fairness, transparency, and cooperation among countries in combatting tax evasion and promoting economic development.

1.6. Impact Assessment and Review:

Conduct periodic evaluations and impact assessments of the wealth tax to assess its effectiveness in achieving redistributive goals, economic stimulus, and revenue generation objectives.

Establish mechanisms for stakeholder consultation, public input, and parliamentary oversight to review the implementation and outcomes of the wealth tax and make necessary adjustments based on empirical evidence and evolving economic conditions.

Section 2: Update of the Estate Tax

2.1. The estate tax exemption threshold shall be lowered to $3.5 million for individuals and $7 million for married couples, with a graduated tax rate ranging from 20% to 55% on estates exceeding these thresholds.

2.2. Revenues generated from the estate tax shall be allocated to public education, healthcare, and environmental conservation efforts.

2.3. Estate Tax Exclusions and Deductions:

Specify certain assets or transfers that may be excluded from the estate tax calculation, such as charitable donations, bequests to spouses, or assets transferred to family-owned businesses or farms.

Provide for deductions or credits for estate taxes paid to state governments, ensuring that taxpayers are not subject to double taxation on the same assets.

2.4. Small Business and Family Farm Exemptions:

Establish exemptions or preferential treatment for small businesses and family farms to mitigate the impact of the estate tax on intergenerational transfers of family-owned enterprises.

Define eligibility criteria and thresholds for qualifying as a small business or family farm, taking into account factors such as revenue, employment, and generational continuity.

2.5. Conservation Easements and Charitable Trusts:

Incentivize conservation efforts and philanthropic giving by allowing deductions or credits for estate taxes paid on assets transferred to conservation easements or charitable trusts.

Encourage the preservation of environmentally sensitive land, historic properties, and cultural heritage sites through tax incentives for estate planning that promotes long-term stewardship and community benefit.

2.6. Estate Tax Planning and Compliance:

Provide guidance and resources for estate tax planning, including estate planning tools, tax shelters, and trusts, to help taxpayers minimize their estate tax liability through legitimate means.

Enhance enforcement measures and penalties for estate tax evasion or abuse, such as undeclared assets, fraudulent valuations, or improper deductions, to ensure compliance with estate tax laws and regulations.

2.7. Economic Impact Assessment and Monitoring:

Conduct economic impact assessments to evaluate the effects of changes to the estate tax threshold and rate structure on wealth distribution, intergenerational wealth transfer, and economic efficiency.

Monitor estate tax revenues and expenditures to track the allocation and effectiveness of estate tax revenues in funding public services, addressing social needs, and achieving broader policy objectives.

Section 3: Value-Added Tax (VAT) Implementation for Corporate Transactions

3.1. A value-added tax (VAT) shall be imposed on corporate transactions, including sales of goods and services, at a rate of 10%.

3.2. The VAT revenues shall be earmarked for investment in infrastructure, renewable energy development, and job creation programs.

3.3. Exemptions and Thresholds:

Define exemptions or thresholds for small businesses or startups with limited revenue or sales volume to prevent undue burden on nascent enterprises and encourage entrepreneurship.

Establish criteria for exempting certain essential goods and services from VAT to mitigate the regressive impact on low-income households and ensure affordability of basic necessities.

3.4. Cross-Border Transactions and International Trade:

Address the treatment of VAT on imports and exports to avoid double taxation or unfair competitive advantages for domestic producers relative to foreign competitors.

Harmonize VAT rules and regulations with international standards and agreements to facilitate trade, minimize administrative barriers, and prevent tax evasion or avoidance through cross-border transactions.

3.5. Sector-Specific Considerations:

Customize VAT implementation for specific sectors or industries, taking into account variations in business models, supply chains, and value-added activities.

Consider sector-specific exemptions, reduced rates, or transitional measures to accommodate unique characteristics or challenges faced by sectors such as agriculture, healthcare, education, and nonprofit organizations.

3.6. Compliance and Administration:

Develop streamlined processes and electronic systems for VAT registration, reporting, and payment to enhance compliance and reduce administrative burdens for businesses.

Invest in training and capacity-building for tax authorities, businesses, and accounting professionals to ensure effective implementation and enforcement of VAT regulations.

3.7. Transparency and Accountability:

Establish mechanisms for transparency and accountability in VAT revenue allocation and expenditure, including regular reporting on VAT revenues collected, allocated projects, and outcomes achieved.

Ensure public oversight and scrutiny of VAT implementation through parliamentary oversight, independent audits, and stakeholder engagement to uphold accountability and promote trust in the tax system.

Section 4: Streamlining Tax Returns and Ending Tax Return Lobby

4.1. The Internal Revenue Service (IRS) shall be responsible for the direct administration and filing of tax returns on behalf of taxpayers, eliminating the need for third-party tax preparation services.

4.2. The IRS shall develop an online platform for taxpayers to access and review their tax information, submit relevant documents, and receive assistance from IRS personnel as needed.

4.3. Free Tax Preparation Services:

Mandate the provision of free tax preparation services by the IRS for taxpayers with simple tax situations, low-income individuals, and elderly taxpayers, reducing reliance on paid tax preparation services and alleviating financial burdens on vulnerable populations.

Expand eligibility criteria for free tax preparation services to include individuals with disabilities, veterans, and other underserved communities, ensuring equitable access to tax assistance and support.

4.4. Taxpayer Assistance and Support:

Enhance taxpayer education and outreach programs to promote awareness of available tax services, rights, and obligations, empowering taxpayers to navigate the tax system independently and confidently.

Establish dedicated helplines, online chat support, and in-person assistance centers staffed by trained IRS personnel to provide personalized guidance, answer inquiries, and resolve taxpayer issues in a timely and efficient manner.

4.5. Data Security and Privacy:

Implement robust cybersecurity measures and data encryption protocols to safeguard taxpayer information and prevent unauthorized access, identity theft, or data breaches.

Ensure compliance with privacy laws and regulations governing the collection, storage, and use of taxpayer data, with strict controls and safeguards in place to protect sensitive personal and financial information.

4.6. Continuous Improvement and Feedback Mechanisms:

Establish mechanisms for ongoing evaluation and improvement of the IRS online platform and taxpayer services, soliciting feedback from users and stakeholders to identify areas for enhancement and address user needs and preferences.

Conduct regular audits and performance reviews of IRS operations, service delivery, and customer satisfaction metrics to monitor progress, identify challenges, and drive continuous improvement in tax administration and taxpayer support.

Section 5: Too Big To Fail - Too Big To Exist Act

5.1. Sectors of the economy deemed "too big to fail" shall be subject to antitrust measures to prevent monopolistic practices and safeguard against systemic risk.

5.2. Institutions identified as "too big to exist" shall be broken up or restructured to promote competition and financial stability.

5.3. Certain sectors, such as banking and residential real estate, shall be nationalized and placed under the jurisdiction of the United States Public Services (USPS - rebadged United States Postal Service), with the aim of providing essential services to all citizens.

5.4. Systemic Risk Assessment:

Establish criteria and thresholds for identifying sectors and institutions as "too big to fail" or "systemically important," taking into account factors such as market share, interconnectedness, and potential impact on the broader economy.

Conduct periodic assessments and stress tests to evaluate the systemic risk posed by large financial institutions and critical infrastructure sectors, informing regulatory decisions and intervention strategies.

5.5. Structural Reforms and Divestitures:

Require "too big to exist" institutions to divest certain assets, subsidiaries, or business lines to reduce their size and complexity, enhancing market competition and resilience to financial shocks.

Mandate structural reforms, such as separating commercial banking from investment banking activities, to mitigate conflicts of interest, prevent excessive risk-taking, and enhance financial stability.

5.6. Public Ownership and Accountability:

Nationalize key sectors or utilities deemed essential to the public interest, such as banking, healthcare, energy, and transportation, under public ownership and control to ensure universal access, affordability, and quality of services.

Establish governance structures and accountability mechanisms for publicly owned entities, including oversight by elected representatives, independent regulatory bodies, and consumer advocacy groups to safeguard public interests and prevent abuses of power.

5.7. Transition and Implementation:

Develop transition plans and timelines for the reorganization or nationalization of "too big to exist" sectors and institutions, allowing for orderly unwinding of existing operations and seamless transition to new ownership or regulatory frameworks.

Provide support and assistance to affected employees, communities, and stakeholders during the transition process, including retraining, job placement services, and economic development programs to mitigate any adverse impacts on employment and local economies.

Section 6: Implementation of PRO Act and Union Protection Measures

6.1. The Protecting the Right to Organize (PRO) Act shall be enacted to strengthen collective bargaining rights, protect workers' ability to organize unions, and penalize employers for anti-union practices.

6.2. Additional measures shall be implemented to promote unionization, including tax incentives for companies with unionized workforces and funding for union education and training programs.

6.3. Union Recognition and Representation:

Strengthen mechanisms for union recognition and certification, ensuring that workers have the right to choose union representation through fair and transparent elections conducted by neutral third parties.

Prohibit employer interference, coercion, or retaliation against workers exercising their rights to join or form a union, including threats, intimidation, discrimination, or termination of employment.

6.4. Bargaining Power and Negotiation Rights:

Enhance collective bargaining rights by requiring employers to negotiate in good faith with recognized unions on wages, benefits, working conditions, and other terms of employment, with meaningful penalties for violations of bargaining obligations.

Expand the scope of bargaining to include issues such as subcontracting, temporary staffing, and technological changes that affect job security and workplace conditions, empowering unions to address emerging challenges and protect workers' interests.

See:

6.5. Worker Participation and Representation:

Establish mechanisms for worker participation and representation in corporate decision-making processes, such as employee representation on corporate boards or works councils, to ensure workers have a voice in shaping company policies and strategies.

Encourage cooperative labor-management relations and joint initiatives to improve productivity, innovation, and workplace culture, fostering a collaborative and inclusive approach to labor relations.

6.6. Union Security and Membership Rights:

Protect union security arrangements, such as union dues checkoff and agency fee arrangements, to ensure stable funding for unions and prevent free-riding by non-members who benefit from union representation and collective bargaining efforts.

Guarantee workers' right to maintain union membership and participation in union activities without fear of discrimination, harassment, or reprisal by employers or fellow employees opposed to unionization.

6.7. Sector-Specific Measures and Protections:

Tailor union protection measures to address specific challenges faced by workers in different industries or sectors, such as gig economy workers, freelance professionals, and precarious workers, ensuring that all workers have access to union representation and collective bargaining rights regardless of employment status or industry affiliation.

Provide targeted assistance and support for organizing efforts in historically marginalized or underrepresented sectors, including low-wage industries, service sectors, and minority communities, to empower workers to assert their rights and improve working conditions.

See:

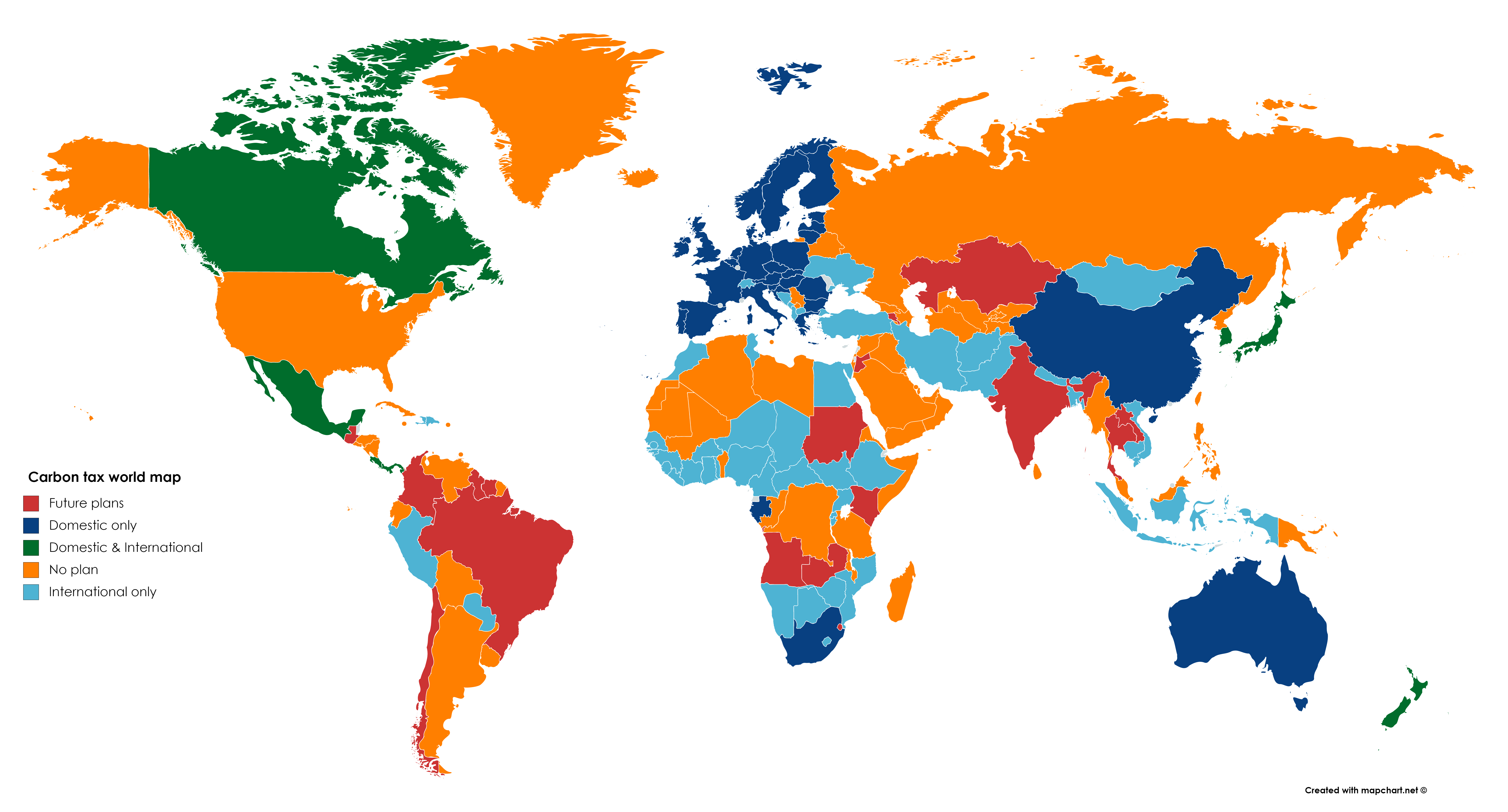

Section 7: Carbon Tax Implementation

7.1. A carbon tax shall be imposed on fossil fuel producers and importers, with rates based on carbon emissions intensity and adjusted annually to reflect environmental impact.

7.2. Revenue generated from the carbon tax shall be invested in renewable energy infrastructure, nuclear and hydrogen energy infrastructure and research, environmental restoration projects, and assistance programs for communities affected by climate change.

7.3. Carbon Tax Rebates and Dividends:

Implement a carbon tax rebate or dividend program to redistribute a portion of carbon tax revenues directly to households, offsetting any potential regressive impacts on low-income families and individuals.

Design the rebate or dividend system to provide greater support to vulnerable populations disproportionately affected by higher energy costs, such as rural communities, indigenous peoples, and marginalized groups.

7.4. Pollution Reduction Incentives:

Allocate a portion of carbon tax revenues for incentive programs to encourage pollution reduction, energy efficiency improvements, and investments in clean technologies and renewable energy sources.

Establish grant programs, tax credits, or subsidies for businesses, industries, and households that adopt sustainable practices, reduce greenhouse gas emissions, and transition to low-carbon alternatives.

7.5. Carbon Offsetting and Mitigation Projects:

Direct carbon tax revenues towards funding carbon offsetting and mitigation projects, such as reforestation, afforestation, and soil carbon sequestration initiatives, to capture and store carbon dioxide from the atmosphere.

Support innovative technologies and research efforts aimed at developing carbon capture and storage (CCS) solutions, carbon-neutral fuels, and other climate mitigation technologies with the potential to reduce emissions and mitigate climate change impacts.

7.6. Climate Resilience and Adaptation Measures:

Allocate resources for climate resilience and adaptation programs to help communities prepare for and respond to the impacts of climate change, including extreme weather events, sea-level rise, and changing environmental conditions.

Invest in infrastructure upgrades, disaster preparedness initiatives, and community-based resilience strategies to build adaptive capacity and enhance the resilience of vulnerable regions and populations.

7.7. International Cooperation and Climate Diplomacy:

Engage in international cooperation and climate diplomacy efforts to promote global action on climate change, including participation in multilateral agreements, carbon pricing initiatives, and technology-sharing partnerships.

Advocate for carbon pricing mechanisms, including carbon taxes or emissions trading schemes, at the international level to create a level playing field for businesses and incentivize emissions reductions on a global scale.

See:

Section 8: Progressive Tax Implementation

8.1. The progressive income tax system shall be reformed to include additional tax brackets for high-income earners, with marginal tax rates ranging from 35% to 70% on incomes exceeding $1 million.

8.2. Capital gains and dividend income shall be taxed at ordinary income tax rates for individuals earning over $1 million annually.

8.3. Wealth Taxation:

Introduce a wealth tax on ultra-high-net-worth individuals (UHNWIs) with net assets exceeding a specified threshold, such as $50 million or more, to address wealth inequality and fund investments in social programs and infrastructure.

Apply progressive rates to wealth tax brackets, with higher rates for larger fortunes, and consider exemptions or deductions for certain assets such as primary residences, retirement accounts, and small businesses to prevent unintended consequences and promote economic mobility.

8.4. Corporate Tax Reform:

Reform corporate tax laws to close loopholes, eliminate tax breaks, and ensure that corporations pay their fair share of taxes based on profits generated in the United States.

Increase the corporate tax rate to levels commensurate with historical norms, taking into account international tax competition and the need for revenue to fund public services and investments.

8.5. Financial Transactions Tax:

Implement a financial transactions tax (FTT) on certain financial transactions, such as stock trades, derivatives, and high-frequency trading, to deter speculative behavior, reduce market volatility, and generate revenue for public purposes.

Design the FTT to target high-volume trading activities by large financial institutions and high-net-worth individuals, with exemptions or reduced rates for small investors and retirement accounts to minimize unintended consequences on ordinary investors and long-term investment strategies.

8.6. Estate Tax Reform:

Strengthen estate tax laws to prevent tax avoidance and evasion through loopholes, valuation discounts, and other strategies used by wealthy individuals to transfer assets to heirs tax-free.

Close loopholes in estate planning techniques such as grantor retained annuity trusts (GRATs), family limited partnerships (FLPs), and dynasty trusts to ensure that large estates pay their fair share of taxes upon transfer to heirs.

8.7. International Taxation:

Combat tax evasion and profit shifting by multinational corporations through international tax avoidance schemes such as transfer pricing, base erosion, and profit shifting (BEPS), by implementing measures to improve tax transparency, cooperation, and information exchange among countries.

Advocate for global tax reforms through international organizations such as the Organization for Economic Cooperation and Development (OECD) to address tax havens, treaty shopping, and other practices that undermine fair and effective taxation of multinational profits.

Section 9: Implementation of a Shortened Work Week with Full-Time Pay

9.1. A four-day workweek shall be established for all full-time employees, with no reduction in pay or benefits.

9.2. The transition to a four-day workweek shall be phased in gradually over a period of three years, allowing employers and employees time to adjust to the new schedule.

9.3. Flexibility and Work-Life Balance:

Provide flexibility in scheduling and work arrangements to accommodate diverse employee preferences and family responsibilities, allowing employees to choose their non-working day or staggered schedules based on individual needs.

Promote work-life balance and employee well-being by encouraging employers to adopt policies and practices that prioritize mental health, leisure time, and personal development outside of the traditional workweek.

9.4. Productivity and Performance Measures:

Implement performance-based metrics and productivity indicators to assess the impact of the four-day workweek on organizational efficiency, employee engagement, and overall business outcomes.

Monitor key performance indicators (KPIs) such as employee satisfaction, absenteeism rates, turnover rates, and productivity levels to evaluate the effectiveness of the four-day workweek in achieving desired objectives.

9.5. Training and Skill Development:

Invest in employee training, skill development, and professional development opportunities to enhance workforce productivity and adaptability in the context of a shortened workweek.

Provide resources and support for upskilling, reskilling, and lifelong learning initiatives to empower employees to thrive in a changing labor market and leverage emerging opportunities for career advancement.

9.6. Economic and Social Impacts:

Conduct economic impact assessments to evaluate the effects of the four-day workweek on employment levels, consumer spending patterns, and overall economic activity, including potential benefits such as reduced commuting costs, increased leisure spending, and improved work-life balance.

Assess the social implications of the four-day workweek on family dynamics, community engagement, and societal well-being, considering factors such as childcare arrangements, volunteerism, and civic participation.

See:

9.7. Stakeholder Engagement and Consultation:

Engage with stakeholders, including employers, employees, unions, industry associations, and government agencies, to solicit feedback, address concerns, and facilitate collaborative decision-making on the implementation of the four-day workweek.

Establish mechanisms for ongoing dialogue, information sharing, and conflict resolution to promote transparency, accountability, and trust in the transition to a shorter workweek.

9.7. Work from Home (WFH) Mandate:

Mandate that work from home (WFH) must be offered as an option to all employees, except where being on premises is a bona fide occupational qualification (BFOQ) necessary for the performance of essential job functions.

Ensure that employers provide the necessary resources, support, and accommodations to enable employees to work remotely, including access to technology, internet connectivity, and ergonomic workspaces.

Require employers to assess employees' home infrastructure and suitability for remote work, taking into account factors such as internet reliability, data security, and the nature of job duties, to determine eligibility for WFH arrangements.

Promote flexibility and work-life balance by allowing employees to choose between on-site and remote work options based on individual preferences, family obligations, and health considerations, while ensuring that business needs and operational requirements are met.

9.4. Transition to Three-Day Work Week Trials:

Mandate that if the transition to a four-day workweek proves successful over a period of 24 months of full implementation, trials for a three-day workweek shall immediately commence.

Set a goal of full transition to a three-day workweek within five years of the commencement of trials, contingent upon the successful outcomes of the trial period, including sustained productivity, employee satisfaction, and business performance.

Require employers to collaborate with employees, unions, and relevant stakeholders to design and implement pilot programs for the three-day workweek, including flexible scheduling arrangements, workload management strategies, and performance metrics to assess feasibility and effectiveness.

Provide support and resources for employers and employees participating in the three-day workweek trials, including training, guidance, and technical assistance to navigate operational challenges, optimize productivity, and ensure smooth transition to the new work schedule.

Monitor and evaluate the impact of the three-day workweek trials on productivity, employee well-being, and organizational outcomes, using feedback from participants, performance metrics, and objective measures to inform decision-making and refine implementation strategies as needed.

Section 10: Implementation of the CROWN Act

10.1. The CROWN Act (Create a Respectful and Open World for Natural Hair) shall be enacted to prohibit discrimination based on hairstyles or hair textures associated with race, ethnicity, or cultural identity.

10.2. Employers, educational institutions, and public accommodations shall be prohibited from enforcing grooming policies or dress codes that disproportionately impact individuals with natural or protective hairstyles, such as afros, braids, twists, locks, or bantu knots.

10.3. The CROWN Act shall require employers and educational institutions to accommodate cultural, religious, or personal grooming practices related to hairstyles, ensuring that individuals are not subjected to adverse treatment or differential treatment based on their natural hair texture or style.

10.4. Enforcement mechanisms shall be established to investigate complaints of discrimination under the CROWN Act, including penalties for violators, remedial measures for victims, and public awareness campaigns to promote compliance and education on natural hair discrimination issues.

10.5. Training programs and resources shall be developed to raise awareness and promote understanding of natural hair diversity, cultural sensitivity, and inclusive grooming practices among employers, educators, students, and the general public.

10.6. The implementation of the CROWN Act shall be monitored and evaluated to assess its effectiveness in preventing natural hair discrimination, promoting diversity and inclusion, and fostering a respectful and open environment for individuals of all racial and ethnic backgrounds.

Section 11: Implementation of Equal Pay for Equal Work

11.1. Equal Pay Principles:

Enact legislation to ensure that all employees receive equal pay for equal work, regardless of gender, race, ethnicity, sexual orientation, gender identity, disability, or other protected characteristics.

Prohibit wage discrimination based on factors such as gender, race, ethnicity, or other protected characteristics, including differences in salary, bonuses, benefits, or other forms of compensation.

11.2. Pay Transparency:

Require employers to provide transparency in compensation practices, including disclosing salary ranges for job positions, pay scales, and criteria used for determining wages, to promote fairness and accountability in pay decisions.

Prohibit employers from retaliating against employees who inquire about, discuss, or disclose their wages or the wages of their colleagues, ensuring that employees have the right to advocate for fair compensation without fear of reprisal.

11.3. Pay Equity Audits:

Mandate regular pay equity audits and assessments to identify and address disparities in compensation based on gender, race, ethnicity, or other protected characteristics, with requirements for corrective action plans to rectify any inequities uncovered.

Provide resources and support for employers to conduct pay equity analyses, implement best practices, and take proactive measures to eliminate pay gaps and promote equitable pay practices.

11.4. Salary History Bans:

Implement salary history bans to prohibit employers from requesting or relying on job applicants' salary history during the hiring process, as such practices perpetuate wage disparities and contribute to systemic discrimination.

Encourage employers to base salary offers on job responsibilities, qualifications, and market rates, rather than past compensation, to ensure that pay decisions are fair, objective, and merit-based.

11.5. Equal Pay Enforcement:

Strengthen enforcement mechanisms to hold employers accountable for pay discrimination, including penalties for violators, remedies for victims of wage disparities, and oversight by regulatory agencies to monitor compliance with equal pay laws.

Provide avenues for individuals to file complaints, seek redress, and pursue legal recourse in cases of pay discrimination, with protections against retaliation for exercising their rights under equal pay laws.

11.6. Education and Awareness:

Promote education and awareness campaigns to inform employers, employees, and the public about the importance of equal pay, the consequences of wage disparities, and the benefits of fair and equitable compensation practices.

Offer training programs, resources, and guidance on pay equity, unconscious bias, and diversity and inclusion in the workplace to empower employers to create inclusive and equitable work environments that promote equal opportunity and economic justice.

Conclusion

This Comprehensive Tax and Economic Reform Act aims to address income inequality, promote economic stability, and ensure the prosperity of all Americans. By implementing progressive tax measures, ending monopolistic practices, and investing in social welfare programs, infrastructure, and environmental sustainability, the United States can build a more equitable and resilient economy for future generations.

See:

I am neither a lawyer nor a financial advisor and this document does not constitute legal or financial advice.

This proposal is a thought exercise and is no guarantee of either product or service.

Contact Your Representatives

Find Your Representative - United States House of Representatives

Contacting U.S. Senators - United States Senate

Find Your Members - CONGRESS.GOV

Find and contact elected officials - usa.gov

Check Your Voter Registration Status

How to confirm your voter registration status - usa.gov

Check Your Voter Registration - Missouri Secretary of State

Written with ChatGPT and checked for plagiarism on plagiarismdetector.net on April 8, 2024.

Previous:

Next:

Return to Start:

Putin Is A War Criminal

Russia Is A Terrorist State:

Part 1 (1990s)

Part 2 (2000s)

Part 3 (2011 - 2016)

Part 4 (2016 - 2019)

Part 5 (2020 - 2021)

Part 6 (2022)

{kind=link}