Deets On Taxing The Church Amendment

Deets On Taxing The Church Amendment

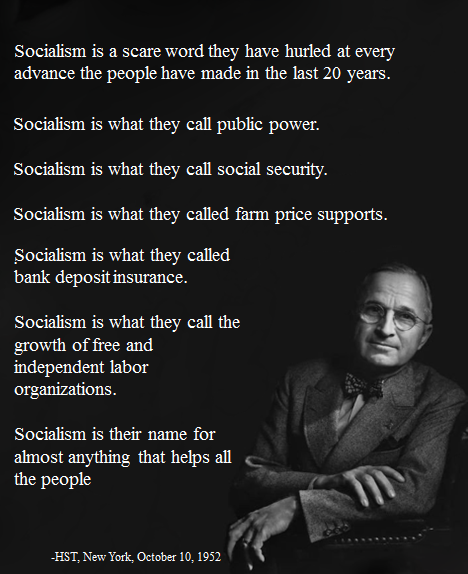

Deets On The Fair Deal

Deets On Taxing The Church Amendment

Deets On Taxing The Church Amendment

Recognizing the need to promote fairness and equity in taxation while addressing critical social welfare needs, we propose this Amendment to revise the tax treatment of religious institutions and allocate revenue generated to fund essential social welfare programs.

Section 1: Revocation of Religious Tax-Exempt Status

1.1. Religious institutions, including churches, mosques, temples, and other places of worship, shall no longer be granted tax-exempt status under federal law. This means that religious organizations will be subject to taxation on their income, property, and other financial activities, similar to other non-religious entities.

1.2. All tax benefits and exemptions previously granted to religious institutions shall be rescinded, including exemptions from income tax, property tax, sales tax, and other forms of taxation. This includes exemptions for religious organizations' real estate holdings, business income, donations, and other sources of revenue.

1.3. Religious institutions will be required to file tax returns and comply with all relevant tax laws and regulations, including reporting requirements, recordkeeping obligations, and payment of taxes owed. Failure to comply with tax laws may result in penalties, fines, or other enforcement actions by the Internal Revenue Service (IRS) or other relevant tax authorities.

1.4. The revocation of tax-exempt status for religious institutions is intended to promote fairness, equity, and neutrality in the tax system by treating religious and non-religious organizations alike. It eliminates preferential treatment for religious entities and ensures that all organizations contribute their fair share to support public services and infrastructure.

1.5. The funds generated from taxing religious institutions will be used to fund essential government programs and services, including education, healthcare, infrastructure development, social welfare, and other public goods. This will help alleviate the tax burden on other taxpayers and ensure that public resources are allocated efficiently and equitably for the benefit of all citizens.

1.6. Religious institutions may still qualify for tax exemptions or deductions under certain conditions, such as engaging in charitable activities or providing services that benefit the public interest. However, such exemptions will be subject to strict scrutiny and eligibility criteria to prevent abuse or exploitation of tax loopholes for private gain.

1.7. The revocation of tax-exempt status for religious institutions does not infringe upon the freedom of religion guaranteed by the First Amendment to the United States Constitution. Religious organizations remain free to practice their faith and engage in religious activities without government interference or discrimination. However, they will be subject to the same legal and financial obligations as other secular entities in the eyes of the law.

Section 2: Taxation of Religious Institutions

2.1. Religious institutions, irrespective of their denomination or religious affiliation, shall be subject to taxation based on their revenue and activities, mirroring the tax obligations of for-profit businesses of comparable size and scope.

2.2. Tax rates applicable to religious institutions shall be determined by assessing their total annual revenue, taking into account various sources of income such as donations, grants, investments, and any revenue generated from commercial activities or business ventures.

2.3. To ensure fairness and equity in taxation, progressive tax rates shall be applied, with higher rates imposed on larger religious institutions with higher revenue streams. This progressive taxation system aims to distribute the tax burden proportionally, reflecting the financial capacity and resources of each institution.

2.4. The determination of tax rates for religious institutions shall consider factors such as the size of the congregation or membership, the scale of the organization's operations and activities, and the extent to which it engages in commercial or profit-generating ventures.

2.5. Taxable income for religious institutions shall encompass all revenue generated from activities unrelated to their core religious functions, including income derived from commercial enterprises, real estate holdings, and investment portfolios.

2.6. Religious institutions shall be required to file annual tax returns, providing detailed financial information and documentation of their revenue sources, expenses, and assets. Compliance with tax laws and regulations shall be monitored and enforced by the Internal Revenue Service (IRS) or other relevant tax authorities.

2.7. Non-compliance with tax obligations, including failure to file tax returns, underreporting of income, or evasion of taxes, shall result in penalties, fines, and other enforcement actions in accordance with applicable tax laws and regulations.

2.8. Tax revenue collected from religious institutions shall be allocated to support public services, infrastructure development, and social welfare programs that benefit the broader community. These funds will contribute to the provision of essential services, such as education, healthcare, public safety, and environmental protection, for the benefit of all citizens.

Section 3: Allocation of Revenue

3.1. Revenue generated from the taxation of religious institutions shall be allocated to support a range of social welfare programs aimed at addressing key societal needs and promoting the well-being of all citizens. The following programs shall receive funding:

(a) Guaranteeing Housing: Significant resources shall be allocated to ensure access to safe, affordable housing for individuals and families facing housing insecurity or homelessness. This funding will support initiatives such as subsidized housing programs, rental assistance, and homelessness prevention efforts aimed at providing stable housing options for those in need.

(b) Improving Prison Conditions: Funds shall be directed towards improving conditions within the prison system, with a focus on infrastructure upgrades, rehabilitation programs, and mental health services. Investments will be made to enhance facilities, provide educational and vocational training opportunities for inmates, and expand access to mental health treatment and counseling services to support inmate rehabilitation and reduce recidivism rates.

(c) Expanding SNAP (Supplemental Nutrition Assistance Program): Increased funding shall be allocated to expand eligibility and benefits under the SNAP program, ensuring that low-income individuals and families have access to nutritious food options. This investment will help alleviate food insecurity and hunger by providing vital assistance to households struggling to afford an adequate diet, thereby improving nutritional outcomes and overall health outcomes.

(d) Expanding TANF (Temporary Assistance for Needy Families): Resources shall be directed towards expanding the TANF program, which provides financial assistance and support services to low-income families with children. This funding will help address the immediate needs of vulnerable families by providing cash assistance, job training, childcare support, and other essential services aimed at promoting self-sufficiency and economic stability.

(e) Subsidizing Healthcare Expenses: Funding shall be earmarked to subsidize healthcare expenses for individuals and families who lack access to affordable health insurance coverage. This investment will help reduce financial barriers to healthcare access by providing subsidies for medical care, prescription medications, preventive services, and other essential healthcare needs, ensuring that all individuals have access to quality healthcare regardless of their income level or insurance status.

By allocating revenue from the taxation of religious institutions to these critical social welfare programs, the government aims to address pressing societal challenges, promote equity and justice, and improve the overall quality of life for all citizens. These investments reflect a commitment to building a more inclusive and compassionate society where everyone has the opportunity to thrive and reach their full potential.

Section 4: Implementation and Enforcement

4.1. The Internal Revenue Service (IRS) shall assume the primary responsibility for the implementation and enforcement of the taxation of religious institutions as outlined in this Amendment. The IRS, as the federal agency tasked with tax administration and enforcement, possesses the requisite expertise and infrastructure to carry out these responsibilities effectively and efficiently.

4.2. The IRS shall develop comprehensive guidelines, regulations, and procedures to govern the taxation of religious institutions in accordance with the provisions of this Amendment. These guidelines shall include clear criteria for determining the tax liability of religious organizations, including the identification of taxable income sources, calculation of tax rates, and assessment of penalties for non-compliance.

4.3. The IRS shall establish mechanisms for monitoring and auditing religious institutions to ensure compliance with tax laws and regulations. This may involve conducting regular financial audits, reviewing tax returns, and verifying the accuracy and completeness of reported income and expenses. The IRS shall have the authority to request documentation, conduct interviews, and take other necessary actions to verify the tax compliance of religious organizations.

4.4. In cases of suspected non-compliance or tax evasion by religious institutions, the IRS shall have the authority to initiate enforcement actions, including imposing penalties, fines, or other sanctions as prescribed by law. The IRS shall exercise its enforcement powers judiciously and impartially, ensuring that all religious organizations are held accountable for their tax obligations in a fair and equitable manner.

4.5. The IRS shall collaborate with other relevant federal, state, and local agencies to facilitate the implementation and enforcement of the taxation of religious institutions. This may include sharing information, coordinating enforcement efforts, and providing technical assistance and support to ensure uniformity and consistency in tax administration across jurisdictions.

4.6. The IRS shall prioritize transparency and accountability in the implementation and enforcement of the taxation of religious institutions, providing regular updates, reports, and disclosures to Congress and the public on its activities and findings. This transparency will help build public trust and confidence in the tax system while promoting adherence to tax laws and regulations by religious organizations.

Section 5: Severability

5.1. In the event that any provision of this Amendment is deemed unconstitutional, invalid, or unenforceable by a court of competent jurisdiction, such a determination shall not affect the validity or enforceability of the remaining provisions of the Amendment.

5.2. The remaining provisions of this Amendment shall continue to remain in full force and effect to the extent permitted by law, and any such invalid or unenforceable provision shall be severed from the rest of the Amendment without prejudice to its overall validity and enforceability.

5.3. The severance of any unconstitutional, invalid, or unenforceable provision shall not impair the intent or purpose of this Amendment, which shall be construed and enforced to the fullest extent possible to achieve its objectives within the bounds of law and constitutional principles.

5.4. Should any provision of this Amendment be severed due to being deemed unconstitutional, invalid, or unenforceable, the parties shall endeavor to negotiate in good faith to replace such provision with a lawful and enforceable alternative that preserves the intent and purpose of the Amendment to the greatest extent possible.

5.5. The severability clause contained herein is intended to ensure that the invalidity or unenforceability of any single provision does not undermine the overall effectiveness or integrity of the Amendment, and that the remaining provisions remain intact and operative to achieve the desired objectives of the legislation.

Section 6: Effective Date

6.1. This Amendment shall come into effect upon its ratification through the Constitutional Amendment Process as outlined in the Constitution of [Insert Applicable Jurisdiction].

6.2. Ratification of this Amendment shall occur following the completion of the requisite procedures specified in the Constitution, which may include approval by a specified majority of both houses of the legislature, ratification by a designated number of state legislatures, or through a constitutional convention, as provided for in the governing legal framework.

6.3. Upon ratification, this Amendment shall be binding and enforceable in accordance with the laws and procedures set forth in the Constitution and other applicable legal statutes and regulations.

6.4. The effective date of this Amendment shall signify the commencement of its legal force and applicability, marking the beginning of the implementation of its provisions and the realization of its intended objectives.

6.5. All governmental bodies, agencies, and individuals subject to the jurisdiction of [Insert Applicable Jurisdiction] shall be obligated to comply with the provisions of this Amendment upon its effective date, and failure to do so may result in legal consequences as prescribed by law.

6.6. The effective date of this Amendment may be subject to any transitional provisions or timelines specified within the Amendment itself or in subsequent legislative or regulatory enactments designed to facilitate its implementation and integration into the existing legal framework.

Conclusion

This Amendment seeks to promote fairness and equity in taxation while addressing critical social welfare needs. By revising the tax treatment of religious institutions and allocating revenue to fund essential social welfare programs, we aim to build a more just and compassionate society where all individuals have access to the resources and support they need to thrive.

See:

#TaxTheChurch

I am neither a lawyer nor a financial advisor and this document does not constitute legal or financial advice.

This proposal is a thought exercise and is no guarantee of either product or service.

Contact Your Representatives

Find Your Representative - United States House of Representatives

Contacting U.S. Senators - United States Senate

Find Your Members - CONGRESS.GOV

Find and contact elected officials - usa.gov

Check Your Voter Registration Status

How to confirm your voter registration status - usa.gov

Check Your Voter Registration - Missouri Secretary of State

Written with ChatGPT and checked for plagiarism on plagiarismdetector.net on April 6, 2024.

Previous:

Next:

Return to Start:

Putin Is A War Criminal

Russia Is A Terrorist State:

Part 1 (1990s)

Part 2 (2000s)

Part 3 (2011 - 2016)

Part 4 (2016 - 2019)

Part 5 (2020 - 2021)

Part 6 (2022)

.jpg){kind=link}